Australian Business Structures: Which Is Best for Tax and Liability?

Which Business Structure Is Best in Australia?

Quick Answer: Australia has four main business structures: Sole Trader, Pty Ltd Company, Partnership and Trust. For most businesses, a Pty Ltd Company offers the best balance of personal liability protection, tax flexibility and credibility. However, the right structure depends on your risk exposure, whether you have partners or investors, your expected revenue, and how you want to distribute income.

- Sole Trader: simplest and cheapest but no personal asset protection

- Pty Ltd Company: separate legal entity with limited liability and 25% tax rate

- Partnership: shared ownership but unlimited personal liability for all partners

- Trust: flexible income distribution but complex and costly to establish

This is one of the most important decisions you’ll make when starting a business. Too many business owners skip it altogether, effectively merging their personal and business interests and leaving themselves exposed. If you’re serious about going into business, you need to take it seriously and structure it properly.

Key Takeaways on Australian Business Structures

- The four business structures in Australia are Sole Trader, Pty Ltd Company, Partnership and Trust. Each has different rules for liability, tax, ownership and compliance.

- A Pty Ltd Company is the best structure for most businesses because it separates your personal assets from business debts and gives you access to the 25% company tax rate.

- Sole Traders have unlimited personal liability. If your business is sued, your house, car and savings are all at risk.

- Partnerships make every partner personally liable for the debts of all other partners. This is one of the riskiest structures.

- Trusts offer flexible income distribution but are complex and expensive to set up. The ATO has been cracking down on trust structures used for tax minimisation.

- You can change your business structure later, but it involves re-registration, transferring assets and potential tax consequences. Getting it right from the start saves time and money.

Business Structure Comparison Table: Australia 2026

The table below compares the four Australian business structures across the criteria that matter most: liability, tax, cost, and suitability.

| Feature | Sole Trader | Partnership | Pty Ltd Company | Trust |

|---|---|---|---|---|

| Separate legal entity? | No | No | Yes | Yes (held by Trustee) |

| Personal liability | Unlimited | Unlimited (all partners) | Limited to company assets | Limited (if Corporate Trustee) |

| Tax rate | Personal rate (up to 45%) | Personal rate (up to 45%) | 25% company rate | Distributed to beneficiaries at their rate |

| Setup cost | Free to low (ABN only) | Low (ABN + Partnership Agreement) | $600 to $900+ (ASIC fees + setup) | $1,500 to $3,000+ (Trust Deed + Trustee company) |

| Ongoing compliance | Low (personal tax return) | Low (partnership return + personal returns) | Medium (company tax return, ASIC annual review) | High (trust return + Trustee company obligations) |

| Can have investors/shareholders? | No | Partners only | Yes (shareholders) | Beneficiaries only |

| Asset protection | None | None | Yes | Yes |

| Income splitting? | No | Between partners only | Via dividends to shareholders | Yes (flexible distribution to beneficiaries) |

| Best for | Solo freelancers, low-risk side businesses | Short-term collaborations, professional practices | Most growing businesses, anyone needing liability protection | Families, asset protection, income distribution planning |

Our recommendation: For most Australian businesses, a Pty Ltd Company offers the best balance of liability protection, tax flexibility and credibility. A Sole Trader is only suitable if your business carries minimal risk and you have no plans to grow beyond yourself.

Click on any headings below to jump to that section of this legal guide.

Legal issues covered in this guide

If you still have a question after reading this guide, get in touch, as we’d love to keep adding your questions to this comprehensive guide.

What Are the 4 Types of Business Structures in Australia?

In Australia, there are generally 4 options for structuring your business.

Sole Trader: A Sole Trader is the simplest and cheapest business structure in Australia. You and the business are legally the same entity. This means your personal assets (including your home) are not protected if your business is sued or is unable to pay its debts. There are no formation costs beyond registering an ABN, and you report business income on your personal tax return.

Pty Ltd Company: A Proprietary Limited (Pty Ltd) Company is a separate legal entity from you. This means your personal assets are protected if the business incurs debts or faces legal action. Only the company’s assets are at risk. You’ll pay the 25% company tax rate on profits (for businesses with turnover under $50 million) rather than personal tax rates that can reach 45%. The trade-off is higher setup costs ($600 to $900+) and ongoing compliance requirements with ASIC and the ATO.

Partnership: A Partnership lets two or more people run a business together and share income. It’s cheaper to set up than a Company, but every partner has unlimited personal liability for all business debts. Critically, each partner is also personally liable for debts incurred by the other partners. The partnership itself doesn’t pay tax. Instead, each partner reports their share of income on their personal tax return at their individual tax rate.

Trust: A Trust is not a business entity itself. It’s a legal structure that holds business assets on behalf of beneficiaries. A Trustee (usually a Pty Ltd Company) manages the Trust and makes decisions. The key benefit is flexible income distribution. The Trust itself pays no tax. Instead, income is distributed to beneficiaries who pay tax at their individual rates. This creates tax planning opportunities that other structures don’t offer. However, Trusts cost $1,500 to $3,000+ to establish, have complex ongoing compliance, and the ATO closely scrutinises trust arrangements.

That’s the summary. Now let’s look at each option in more detail.

Sole Trader Pros and Cons

As a Sole Trader, your personal assets (e.g. your house) are at risk.

A Sole Trader immediately comes to mind when most people think of a small business owner. The Sole Trader structure is for individuals doing business on their own. This structure preserves your right to make all decisions about your business but clouds any distinction between your personal and business assets.

The costs of becoming a Sole Trader are minimal, and the application process is relatively simple compared to other business structures. Ongoing administration costs are also smaller. If all this sounds too good to be true, it might be.

Sole Traders are not wholly separate legal entities from their owners, which means that if your business is sued, you could end up paying the costs from your personal assets. You’ll also be stuck personally with your business debts, including any tax obligations incurred.

In addition, being a Sole Trader doesn’t offer you any real tax benefits (vs a Pty Ltd company). All-in-all, this business setup is less than ideal.

Can I change from Sole Trader to Pty Ltd?

Yes. You can change your business structure from a Sole Trader to a Pty Ltd Company at any time. Many Australian business owners start as Sole Traders and transition once their revenue grows or they need liability protection. Here are the key steps:

- For Pty Ltd companies and Partnerships, you must register your new business structure with the Australian Government Business Registration Service.

- You may need to update the licenses or permits for your new business structure.

- You must inform your bank, insurance providers, etc. about your name change and business structure in Australia.

- Inform your clients and suppliers and update existing contracts, agreements, or business arrangements.

- Transfer assets, liabilities, and other relevant items from your Sole Trader business to the new entity. Be sure to consult your accountant about any tax implications.

- Once the transition is complete, deregister your Sole Trader business.

Does being a Sole Trader affect access to finance and investment?

Unfortunately, yes. Being a Sole Trader has advantages, such as simpler regulatory requirements, lower setup costs, and greater control over the business. But access to finance and investment is limited because of the following factors:

- As a Sole Trader, the business is owned and operated by a single individual, which means there is no legal provision for issuing shares or equity to investors.

- Lenders perceive Sole Traders as higher-risk borrowers, making it more challenging to obtain loans or credit.

- Since a Sole Trader’s business and personal finances are not legally separate, the business owner’s credit history plays a significant role in obtaining financing.

- Lenders may require personal assets as collateral, increasing the personal risk for the business owner.

What are examples of Sole Trader businesses in Australia?

Common examples of Sole Trader businesses in Australia include:

- freelance writers

- graphic designers

- personal trainers

- photographers

- tutors

- tradespeople (plumbers, electricians, carpenters)

- market stall operators

- rideshare drivers, and

- consultants working independently

Sole Trader works well for these businesses because they typically involve one person delivering a service, carry relatively low liability risk compared to product-based businesses, and don’t require significant capital investment. According to the Australian Bureau of Statistics, approximately 1.5 million sole traders are operating in Australia as of June 2024, making it the most common business structure by number.

However, if any of these businesses grow to the point where they’re earning significant revenue or face meaningful liability risk (for example, a trades business taking on large renovation projects), the Sole Trader structure becomes a liability rather than a convenience. That’s when transitioning to a Pty Ltd Company makes sense.

Pty Ltd Company Pros and Cons

A Pty Ltd Company protects you from being personally liable.

If you’re serious about starting and growing a successful business in Australia, you should consider a Pty Ltd Company structure. This is a legal entity that is separate from you personally. If things do go wrong, your business mistakes are unlikely to destroy your personal financial assets. But for this to work successfully, you must keep your personal assets separate from your business assets – separate personal and business bank accounts, family home in your name, not the Company’s, etc.

If you incorporate as a Company, you’ll be a shareholder. You can be the sole shareholder or have multiple shareholders in your business. If you have multiple shareholders, they will usually have a vote on any significant decisions in your business. The voting rights and how your business is managed will be set out in your Company Constitution – a standard document in most cases – and your Shareholder Agreement. The Australian Corporations Act sets out the rules you must adhere to when managing your Company.

The primary drawback of using a Pty Ltd Company is that the formation and ongoing costs are relatively high.

An affordable option for incorporating your Pty Ltd Company (which you can do easily online) is $1,249 through Incorporator.com.au or $661 through Company123.com.au (introductory price, may not last). This includes the ASIC company registration fee of $636. Bear in mind some accountants charge 2-3 times this amount.

Then you’ll need to file a company tax return with the ATO annually and update your ASIC registration details. The costs of an accountant to prepare and submit your personal and company tax returns can run between $1,000 and $2,500, depending on the complexity of the return and whether your accountant is located in a major Australian city or regional town. In addition, you’ll need to pay the annual ASIC Review Fee, which is $342 from 1 July 2026.

But a Company structure does give you some ability to structure your earnings from the business in the most tax-effective way.

What does Pty Ltd mean?

Pty Ltd stands for “Proprietary Limited”. In this context, “Proprietary” refers to the private ownership and control of the company, distinguishing it from a public company with shares traded on a public stock exchange. And “Limited” refers to the limited liability of the company’s shareholders. Limited liability means that shareholders are not personally liable for the company’s debts or legal obligations beyond the value of their shares.

Pty Ltd vs Sole Trader: Which Should You Choose?

A Pty Ltd Company protects your personal assets. A Sole Trader does not. That’s the fundamental difference, and for most businesses it’s the deciding factor.

Choose Sole Trader if:

- You’re testing a business idea with minimal financial risk

- Your annual revenue is under $75,000

- You work alone and don’t plan to bring in partners or investors

- Your business doesn’t expose you to significant liability (e.g. consulting, freelance writing)

Choose Pty Ltd Company if:

- Your business revenue exceeds $75,000 (you’ll benefit from the 25% company tax rate vs personal rates up to 45%)

- You want to protect your home, car and personal savings from business debts

- You plan to bring in partners, shareholders or investors

- Your business involves products, physical services, or anything that could result in legal claims

- You want to build business credit and credibility separate from your personal finances

The Pty Ltd structure costs more to set up and maintain. Budget $600 to $900 for formation and $1,000 to $2,500 per year for accounting and compliance. But for any business with real revenue and real risk, that cost is a small price for the protection it provides.

Partnership Pros and Cons

With a Partnership, you are liable for all partners’ actions and debts.

If you have a business partner you trust and want to work with; a Partnership might seem like a good choice. For many Australian business owners, this approach works well. The costs of setting up a Partnership are relatively low and the annual administrative costs are less than a Pty Ltd Company. A Partnership also offers greater financial reporting privacy than a (Pty Ltd or Public) Company.

Fun fact about Partnerships …

Generally speaking, a Partnership is limited to between 2 and 20 partners. However, there are exceptions laid out in the Australian Corporations Act. For example, a Partnership can consist of the following:

- 50 Actuaries, Medical Practitioners, Patent Attorneys or Stockbrokers

- 100 Architects, Pharmaceutical Chemists or Veterinary Surgeons

- 400 Legal Practitioners, and

- 1,000 Accountants!

A Partnership also allows you to pool your assets, making it easier to operate your business. For example, if you and your partner apply for a loan for office space, pooling your assets can make you (together) a more attractive loan candidate.

However, Partnerships offer little protection if things go wrong.

You’ll be personally liable for your business debts and lawsuits from poor business decisions. Worse still, in the same way, a Partnership allows you to merge your assets with your partner, you may also be liable for your partner’s debts. These risks can be mitigated with appropriate insurance coverage or by becoming a “limited” partner. For these reasons, we strongly advise anyone considering a Partnership to seek professional advice and to gain a very detailed understanding of your partners’ financial situation.

In addition, Partnerships do not offer any substantial tax benefits. Your Partnership doesn’t pay taxes directly. Instead, you and your partners must lodge annual tax returns and pay personal tax based on your share of the Partnership’s earnings.

Partnership vs Pty Ltd Company?

Here is a summary of the Partnership vs Pty Ltd company structures:

- Legal entity: A Partnership is an arrangement in which two or more individuals or entities jointly own and operate a business. The partners share profits and losses, and there is no legal distinction between the partners and the business itself. A Pty Ltd company is a separate legal entity from its owners, meaning it has its own assets, liabilities, and obligations.

- Liability: In a General Partnership, all partners have unlimited liability for the business’s debts and legal obligations, meaning their personal assets are at risk if the business faces financial or legal issues. In a Limited Partnership, some partners may have limited liability. Pty Ltd company shareholders have limited liability, meaning their personal assets are generally protected if they incur debts or face legal issues.

- Ownership and control: Decision-making is typically shared among partners based on their ownership stakes and the partnership agreement. This can result in collaborative decision-making but may also lead to disagreements or slower decisions. A Pty Ltd company is owned by shareholders and managed by directors. Shareholders can be individuals or other entities, and the number of shareholders is limited.

- Taxation: The Partnership itself does not pay tax on its income. Instead, each partner reports their share of the partnership’s income and pays tax at their personal income tax rates. The Pty Ltd company pays corporate tax on its profits, and shareholders may be taxed on dividends they receive.

- Compliance requirements: Partnerships generally have fewer reporting, record-keeping, and regulatory requirements than Pty Ltd companies.

Sole Trader vs Partnership: What Changes?

Converting from a Sole Trader to a Partnership means sharing ownership, profits and decision-making with one or more other people. You’ll also share liability, and that’s the critical point most people miss.

In a Partnership, you are personally liable not just for your own business debts, but for debts your partners incur on behalf of the business. If your partner signs a bad contract or takes on debt, you’re on the hook too.

A Partnership doesn’t provide the asset protection of a Pty Ltd Company. Before forming a Partnership, consider whether a Company structure with multiple shareholders would offer the same collaboration benefits while providing better liability protection.

If you do proceed with a Partnership, get a detailed Partnership Agreement in writing. This should cover profit sharing, decision-making authority, what happens if a partner wants to leave, and how disputes are resolved. Never rely on a verbal agreement.

Trust Pros and Cons

Trusts do not have the tax advantages they used to.

Trusts are among the oldest legal structures and have been used to handle everything from family inheritances to funding political activities. A Trust is simply an arrangement wherein an overseer, known as a Trustee, manages assets. If you entrust your business to a Trustee, it will act as a business manager, making decisions, disbursing funds and paying bills.

The Trust provides asset protection and limits liability from operating the business. Beneficiaries (owners) of a Trust are generally not liable for Trust debts, unlike Sole Traders and Partnerships. And the Trustee is typically incorporated as a Pty Ltd Company to give the Trustee some protection from liability, too.

The main benefit of operating a Trust is that it gives you flexibility in how income from the Trust is distributed.

The Trust usually pays no tax but distributes its profits to the Beneficiaries yearly. This gives you some tax planning flexibility (taking advantage of the different tax-free thresholds and personal tax rates of each Beneficiary) that the other business structures aren’t able to. However, because Trusts have historically been widely used for tax avoidance, the ATO has been cracking down on Trusts.

The setup and administration of a Trust are very complex and costly. You’ll have to draw up a Deed of Trust, which requires a lawyer’s assistance. And if you want to expand your business and retain profits to do so, you’ll be subject to penalty tax rates.

If you use the Trust option, you’ll likely also use a Corporate structure for the Trustee and/or Beneficiaries, which incurs additional costs.

Business Trust vs Sole Trader?

Here is a summary of the business Trust vs Sole Trader structures:

- Legal entity: A business Trust is a legal arrangement in which the Trust holds and manages the business’s assets and operations on behalf of the beneficiaries. The Trust is a separate legal entity from its trustees and beneficiaries. A Sole Trader operates as an individual, and there is no legal distinction between the business owner and the business itself.

- Liability: Trustees have limited liability for the Trust’s debts and legal obligations, depending on the specific trust structure and terms. Beneficiaries generally have limited liability, as their exposure is usually limited to their interest in the Trust. The Sole Trader has unlimited liability for the business’s debts and legal obligations, meaning their personal assets are at risk if the business faces financial or legal issues.

- Ownership and control: The Trust is managed by one or more trustees, who have a fiduciary duty to act in the best interests of the beneficiaries. Decision-making authority typically rests with the trustees. The Sole Trader business is owned and managed by a single individual, making decision-making quicker and more flexible.

- Taxation: The Trust itself is not taxed on its income; instead, the beneficiaries are taxed on their share of the Trust’s income when distributed. The Sole Trader’s business income is taxed at their personal income tax rates.

- Compliance requirements: A business Trust often has more complex reporting, record-keeping, and regulatory requirements than a Sole Trader. Establishing a Trust can also be more expensive and time-consuming.

Trust vs Company: Which Is Better for Your Business?

Both a Trust and a Pty Ltd Company provide asset protection and limit your personal liability. The key difference is how income is taxed and distributed.

A Pty Ltd Company pays the 25% company tax rate on profits. You then pay personal tax on any dividends you take. A Trust distributes income directly to beneficiaries, who pay tax at their individual rates. This means a Trust can be more tax-effective if you have family members in lower tax brackets.

Choose a Company if:

- You want a straightforward structure with clear ownership via shares

- You plan to retain profits in the business to fund growth

- You want to bring in external investors or sell equity

- You want simpler compliance requirements

Choose a Trust if:

- You have family members who could receive income distributions at lower tax rates

- Asset protection across generations is a priority

- You’re willing to pay higher setup costs ($1,500 to $3,000+) and ongoing compliance

- You understand and accept that the ATO scrutinises trust arrangements closely

Many business owners use both. A common structure is a Discretionary (Family) Trust with a Corporate Trustee (Pty Ltd Company). This gives you the income distribution flexibility of a Trust with the liability protection of a Company for the Trustee. However, this structure involves establishing both entities and maintaining compliance for both, so it’s significantly more expensive.

How to Choose the Right Business Structure in Australia

Choosing the right business structure comes down to four factors: your liability risk, whether you have partners or investors, your expected income, and the level of complexity you can manage.

Step 1: Assess Your Liability Risk

If your business could be sued (you sell products, provide physical services, give professional advice, or handle client money), you need a structure that protects your personal assets. That means a Pty Ltd Company or a Trust with a Corporate Trustee. A Sole Trader or Partnership leaves everything you own exposed.

Step 2: Consider Partners and Investors

If you’re going into business alone, a Sole Trader or single-director Pty Ltd Company are your main option. If you have business partners, a Pty Ltd Company with a Shareholder Agreement gives you better protection than a Partnership. If you plan to raise investment, a Company is the only practical option.

Step 3: Evaluate Your Tax Position

Once your business income exceeds approximately $75,000, the 25% company tax rate becomes more favourable than personal income tax rates. If you have family members in lower tax brackets and want to distribute income to them, a Trust structure may offer additional benefits. Talk to your accountant about the specific numbers for your situation.

Step 4: Factor In Costs and Complexity

A Sole Trader costs almost nothing to set up. A Pty Ltd Company costs $600 to $900 to form, plus $1,000 to $2,500 per year in accounting and compliance. A Trust costs $1,500 to $3,000+ to establish, plus ongoing costs to maintain both the Trust and its Corporate Trustee.

If you’re just starting out with a low-risk service business and minimal revenue, starting as a Sole Trader and transitioning to a Company later is a reasonable approach. But if you’re earning real revenue or facing real liability risk from day one, start with the Company structure. The cost of restructuring later (and the risk of operating without protection) far outweighs the setup costs.

Business Structure Tax Comparison: Australia 2025-2026

Tax is one of the most important factors when choosing a business structure. Here’s how each structure is taxed in Australia.

| Structure | How Income Is Taxed | Tax Rate | Key Tax Feature |

|---|---|---|---|

| Sole Trader | Business income added to your personal income | 0% to 45% (progressive) | No income splitting. All profit taxed at your personal rate. |

| Partnership | Each partner’s share added to their personal income | 0% to 45% per partner | Partnership doesn’t pay tax. Partners each lodge personal returns. |

| Pty Ltd Company | Company pays tax on profits. Dividends taxed personally. | 25% company rate (turnover under $50M) | Can retain profits in the company at 25%. Franking credits offset double taxation on dividends. |

| Trust | Trust distributes income to beneficiaries | Beneficiaries’ individual rates | Flexible distribution. Can allocate income to beneficiaries in lower tax brackets. Undistributed income taxed at 47%. |

Example: If your business earns $120,000 in profit and you’re the only owner:

- As a Sole Trader, you’d pay approximately $31,717 in tax (2025-26 rates, before Medicare levy)

- As a Pty Ltd Company, the company pays $30,000 in tax. You could then pay yourself a salary or dividends, depending on your personal needs, potentially reducing your overall tax burden

- As a Trust distributing to a spouse in a lower bracket, you could split the income and reduce the combined tax paid

These are simplified examples. Your actual tax position depends on deductions, other income, and your personal circumstances. Always consult your accountant before choosing a structure based on tax alone.

Business Registration Requirements

Now, you need to register your business.

Once you’ve decided on the best business structure in Australia for your business and chosen a business name, you need to register your business and business name. And you need to do this with several different Australian regulators and organisations.

Fun fact about Registrations …

Irrespective of whether you’ve chosen to be a Sole Trader, Partnership, Trust or Pty Ltd Company, you will need the following:

- Registered business name

- ABN (Australian Business Number)

- TFN (Tax File Number)

and will probably need to register for GST too. So there are no differences between the various Australian business setup options here.

ASIC: First, you need to sign up for an ASIC Connect account. You should have already searched the ASIC and IP Australia databases to make sure your business name has not previously been registered or trademarked. The ASIC business name registration fee is $47 for one year or $108 for three years (from 1 July 2026). You’ll be given an ACN (Australian Company Number) when your application is approved.

Australian Business Register: Next, you must take your ACN and apply for an ABN (Australian Business Number). An ABN has become a very important unique identifier of your business (necessary for opening bank accounts, filing tax returns, including on invoices, etc.), and every Australian business needs one. At the same time, you can register on this Australian Government website for your TFN (Tax File Number), PAYG (Pay As You Go) and GST. There are no registration fees for these registrations.

IP Australia: This step is often skipped by startup businesses but is vital for protecting your business, brand name and intellectual property. Although you have registered your business name with ASIC, this does not mean you have exclusive ownership. It can be used as a “trading as” name, “Pty Ltd” name or trademarked as a brand name. To prevent this, register your business name (and logo and tagline) with IP Australia. The costs of doing this vary depending on the number of “product categories” you want to cover, but you should expect to spend between $500 and $700 for this extra protection.

Website Domain & Social Media: You also need to register your business online; nowadays, that doesn’t just mean a website address. It includes all the major social media platforms, too! Register your “.com.au” domain and all its derivatives (e.g., .com, .org, .net, .mobi, .info, etc.) with a service like Webcentral (formerly Netregistry). And use NameChk to check whether your business name is available on social media platforms like Facebook, Twitter, and YouTube. Registering on ALL these social media platforms isn’t absolutely necessary, but at least have the majors covered.

Regulatory Licences & Permits: Whether this step is required depends on your business type. The Australian Business Licence and Information Service are like a one-stop shop for finding out what Australian licences, permits, approvals, registrations, etc. your business needs to meet its compliance obligations. Make sure you check it out!

For a step-by-step explanation of how to register your business, see our easy-to-understand infographic: How to Register an Online Business in Australia.

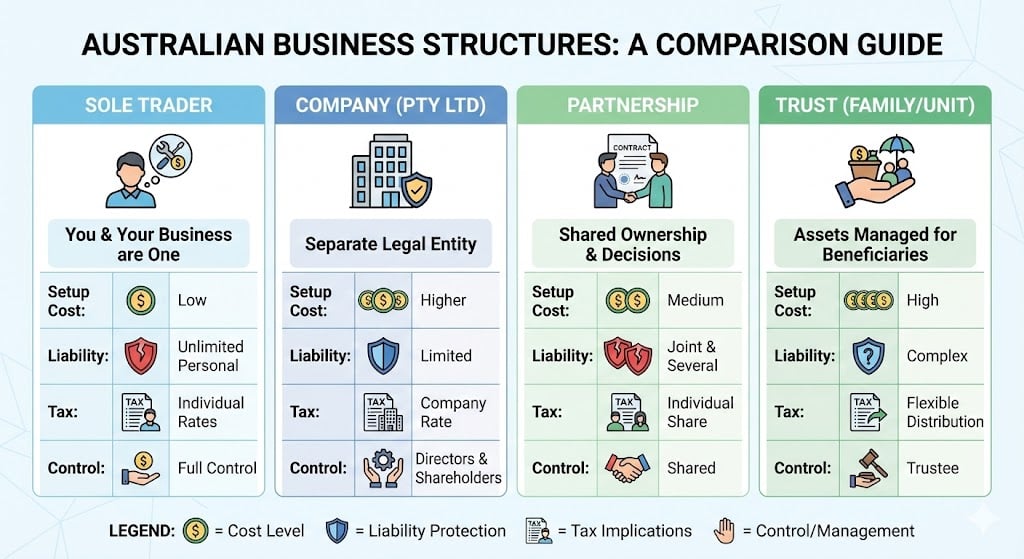

Summary of Business Structure Options

The infographic above summarises the pros and cons of the different Australian business structures, comparing costs, personal liability, tax, and control.

For most Australian businesses, a Pty Ltd Company is the best structure. It protects your personal assets, gives you access to the 25% company tax rate, lets you bring in shareholders, and separates your business and personal finances.

You can change your business structure later. But changing involves re-registration with ASIC, transferring assets and contracts, updating your ABN, informing your bank and insurers, and potentially triggering capital gains tax or stamp duty. It’s not a simple process.

Get the structure right during the startup phase. The cost of setting up a Pty Ltd Company ($600 to $900) is a fraction of what it costs to restructure later. If you need help choosing the right business structure, talk to a lawyer and an accountant before you register.

If you need help choosing the right business structure in Australia and registering your Australian business, get in touch.

About the Author: Vanessa Emilio

Need legal documents written specifically for your business? Vanessa and her team draft custom legal documents for Australian online businesses, or you can book a 30-minute call to talk through what you need.

Disclaimer: We hope you found this article helpful, but please be aware that any information, comments or recommendations are general in nature, do not constitute legal advice and may not be suitable for your specific circumstances. Whilst we try our best to ensure that the information is accurate, sometimes there may be errors or new information that has yet to be included. Any decisions you take based on information on this website are made at your own risk and we cannot be held liable for any losses you suffer. Contact us directly before relying on any of this information.

Book a 30-minute Call with Legal123

Need help with your business from an experienced legal professional? Then book a call with Vanessa Emilio, Practice Director of Legal123.

- Australian lawyer with 20+ years experience

- Ideal for entrepreneurs & business owners

- Advice tailored to your circumstances

- Quick answers to pressing legal questions

- Confidential discussion

- Easy online booking

30-minute Call with Vanessa Emilio, Practice Director $99 +GST